For any lending business, loan recovery is one of the most important parts of the lending process. Bad loans hurt the loan book and increase non-performing loan rates.

Though lenders use several recovery methods to ensure repayments, a significant percentage of repayment failures happens not because customers refuse to pay, but because customer funds are fragmented across multiple accounts. The problem isn’t about customers’ willingness to repay; it’s about where the money sits.

Today, customers rarely own a single bank account. Their funds are often distributed across salary accounts, savings accounts, digital wallets, and mobile money bank accounts. While this flexibility works perfectly for customers, it creates a major challenge for lenders and businesses trying to collect recurring payments.

Most traditional debit systems were also designed for a single authorized account; once the primary account has insufficient funds, the entire repayment process breaks down, even if the customer still has sufficient balances spread across other accounts.

This leads to:

Failed repayment attempts

Increased Days Past Due (DPD)

Manual reminder cycles

Higher operational costs

Delayed revenue recovery

As users’ financial behaviours evolve, repayment systems must evolve as well. What lenders and businesses need is not more payment retrials, but smarter access to customer liquidity across their multiple accounts.

This is why we built Mono Sweep.

What is Mono Sweep, and how does it work?

Mono Sweep is a smart money-sweeping service that enables lenders and businesses to securely collect recurring payments from any bank accounts linked to a customer’s BVN, through a single consent flow.

Instead of relying on a single account for repayments, Mono Sweep allows you to easily initiate debit attempts across multiple approved accounts belonging to the same customer, with their explicit permission.

With traditional debit systems, relying on a single account with insufficient funds leads to more repayment failures.

With Mono Sweep:

The primary account is attempted first

If funds are unavailable, a debit on approved linked accounts is automatically attempted

Collection succeeds without manual retries or intervention

Lenders no longer need to depend on debits to one account, because with your borrower’s consent, repayments happen wherever liquidity exists.

How businesses can use Mono Sweep

Loan and BNPL repayments

Lenders and BNPL services can use Mono Sweep to collect repayments across multiple linked customer accounts.

For example, Ada takes a N300,000 personal loan from a loan app and authorizes her salary account for repayments during the application process. Each month, as soon as her salary is paid into this account, she transfers most of it into another account she uses for savings and daily spending.

On repayment day, the lender attempts to debit the authorized account, but the transaction fails due to insufficient funds, though Ada has enough money elsewhere. Her repayment becomes overdue, pushing her into Days Past Due (DPD) and triggering collection reminders.

With Mono Sweep, funds are automatically recovered from another funded account. The system checks the primary account and proceeds to other linked accounts until recovery succeeds. Ada remains current on repayments while the lender prevents early delinquency.

Subscription-type and contract-based payments

Besides lenders, Mono Sweep is useful for SaaS (Software as a Service) platforms that collect contract-based recurring payments, where customers are obligated to keep paying over a period for ongoing access.

These also apply to subscription license agreements, typically used in the IT sector, where users pay for a license to access software rather than buying it outright. In these cases, though value is delivered over time, the customer is still expected to keep paying for the stipulated duration. So missed payments can disrupt service and affect revenue consistency.

For example, a user signs a 12-month SaaS contract billed monthly. Over time, they switch spending to another account, and the primary account is underfunded. When renewal attempts are made, payments will fail even though funds are available elsewhere.

Mono Sweep improves payment collection by ensuring these businesses can intelligently debit multiple linked accounts with sufficient funds. This results in fewer failed payments, lower churn risk, and more predictable revenue.

Benefits of using Mono Sweep

Mono Sweep directly addresses the operational challenges created by fragmented customer funds and provides these benefits:

Lenders can recover loans faster, improving their repayment success rates and reducing their non-performing loans (NPLs).

Scheduled payments go through more successfully across multiple funded accounts, and retry cycles are fewer.

On-time collections improve, keeping revenue consistent and predictable for SaaS businesses.

Lenders can move away from using manual recovery methods like constant reminders or field recovery agents to collect repayments, keeping operational costs lower.

Pricing

Setup Fee: ₦500 (one-time)

Mandate Activation Fee: ₦100 per linked account

How to get started with Mono Sweep

For existing users

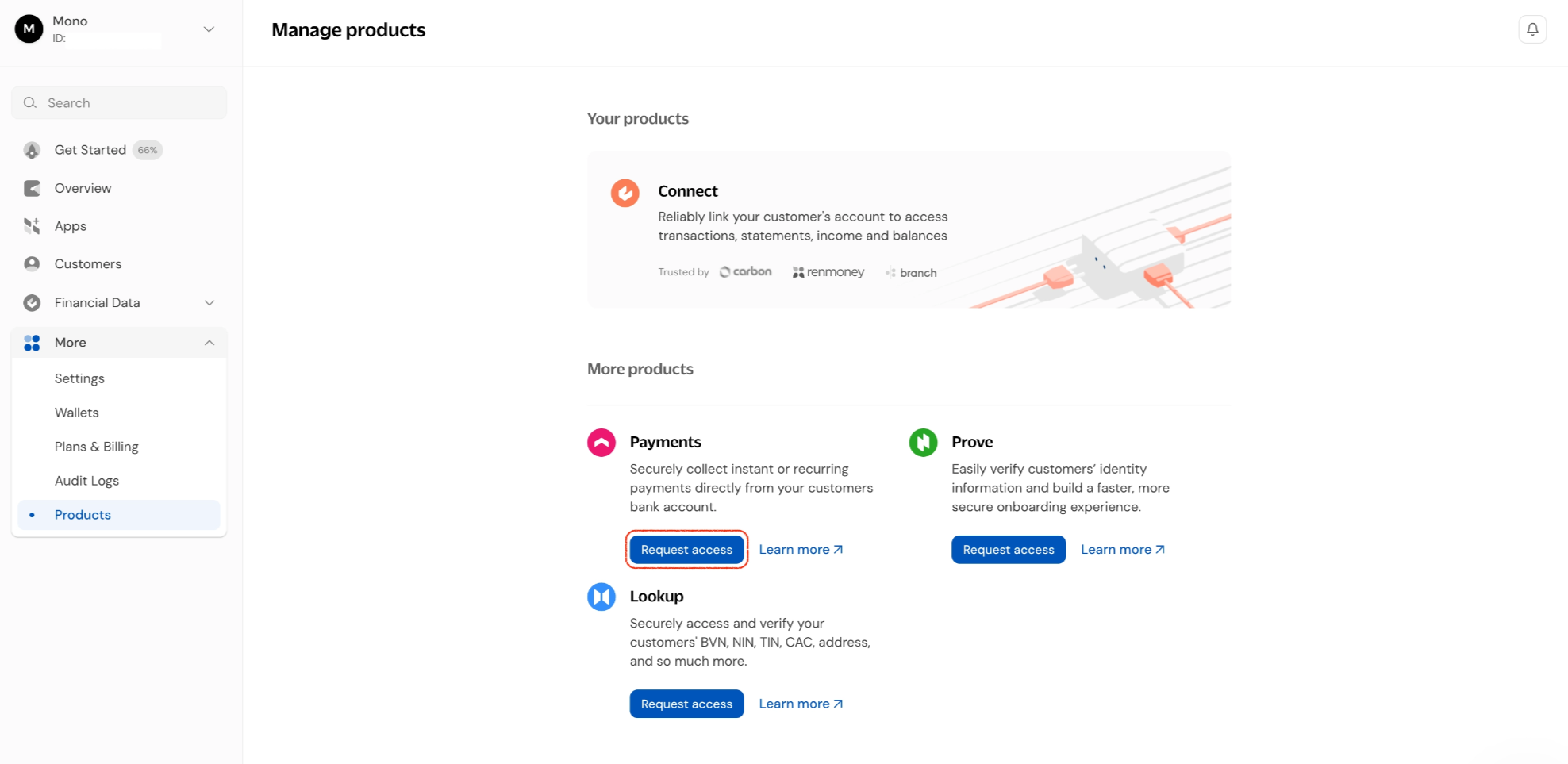

If you already use Mono, you can request access to Sweep directly from your dashboard. Navigate to Products → Payments and click the ‘Request access’ button

For new users

If you’re new to Mono, sign up here to get started, then request access to Mono Sweep. From there, you can either follow our integration guide to use the Mono Sweep APIs or set up and manage Sweep mandates via the Mono dashboard.

For partners already using direct debit mandates

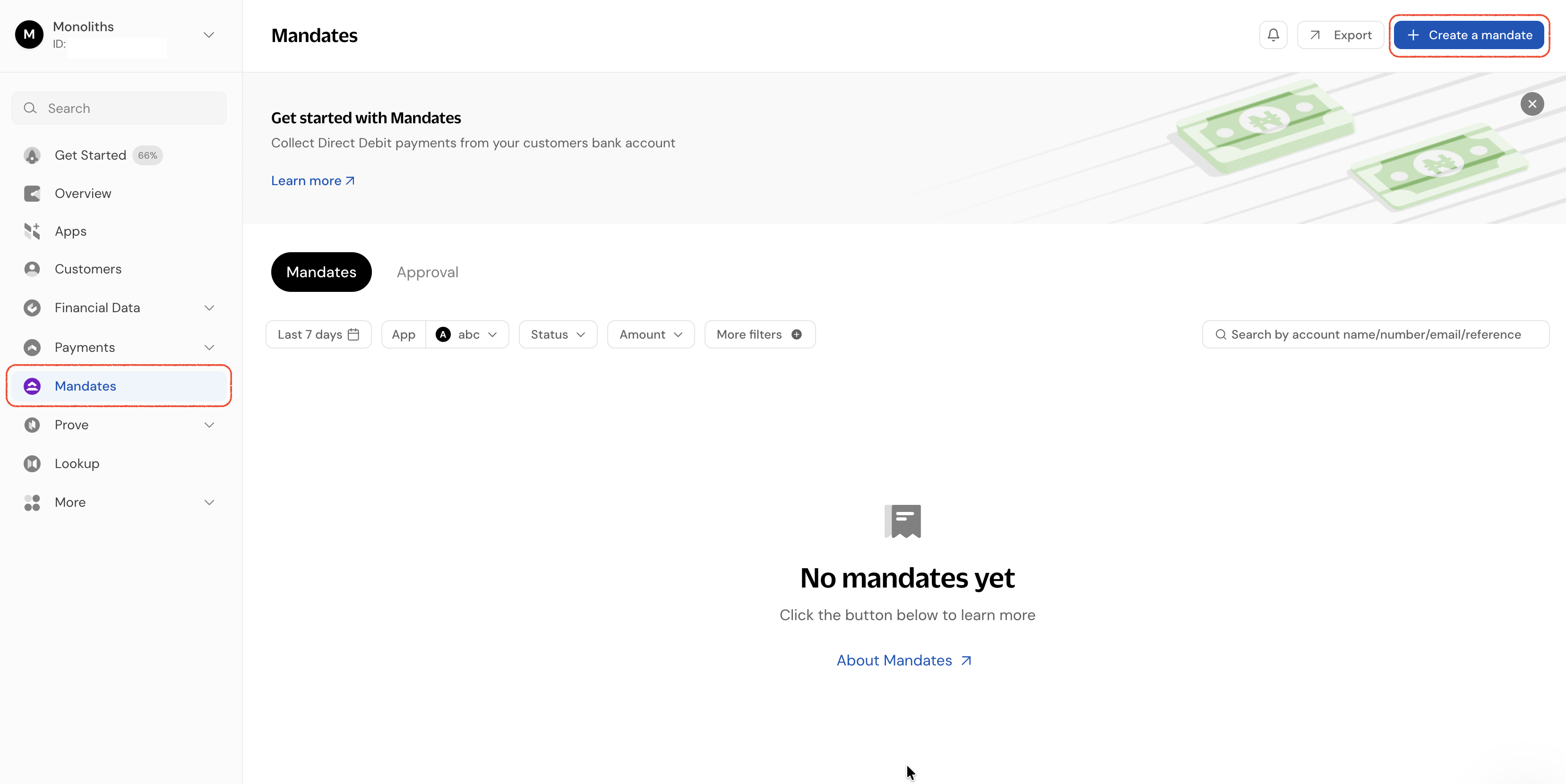

If you have access to direct debit but haven’t enabled Sweep yet, here’s how to do it:

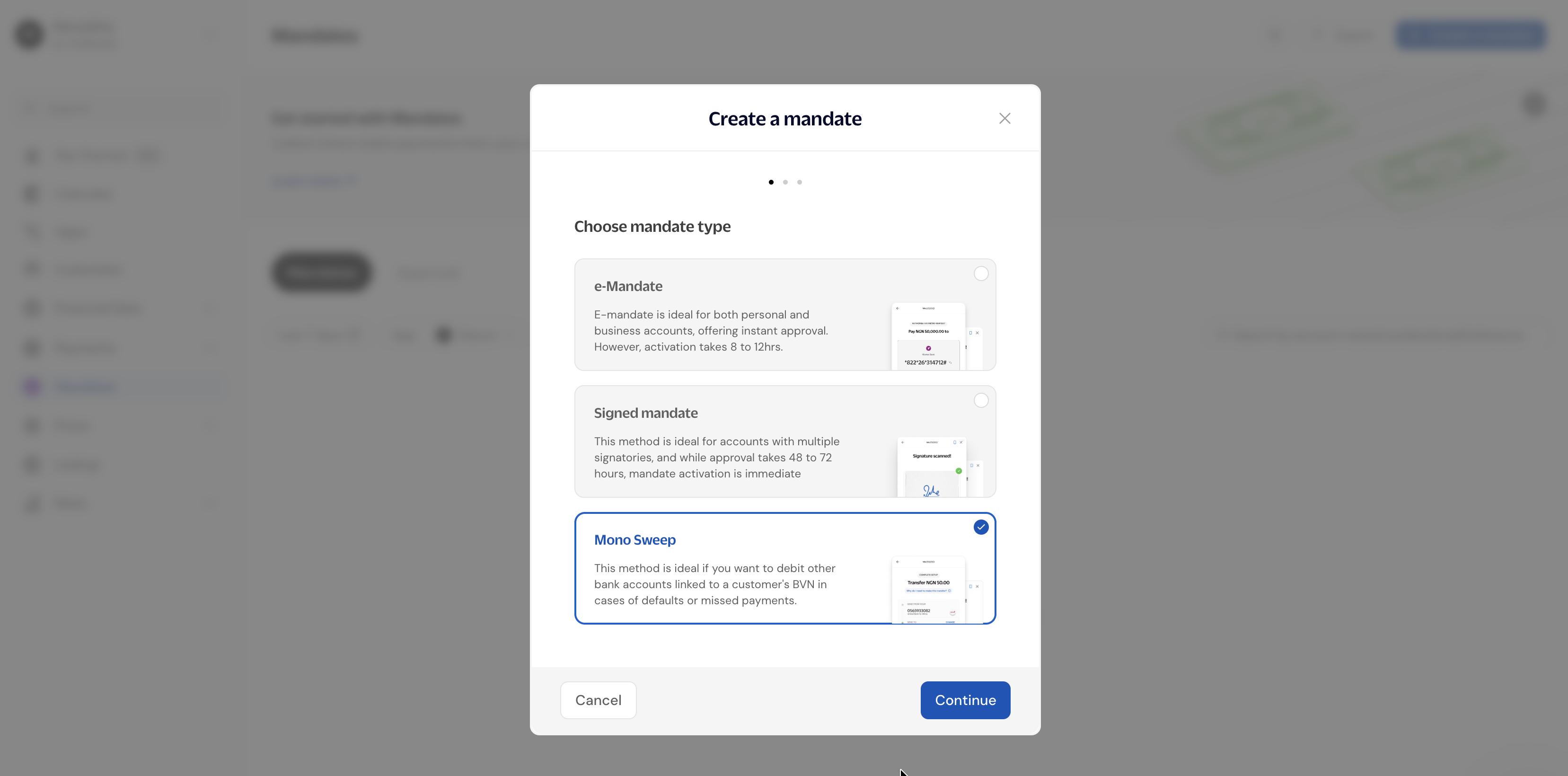

Go to the Mandates option on the sidebar menu and click the ‘Create a mandate’ button at the top right.

On the pop-up menu, select the Mono Sweep option to continue.

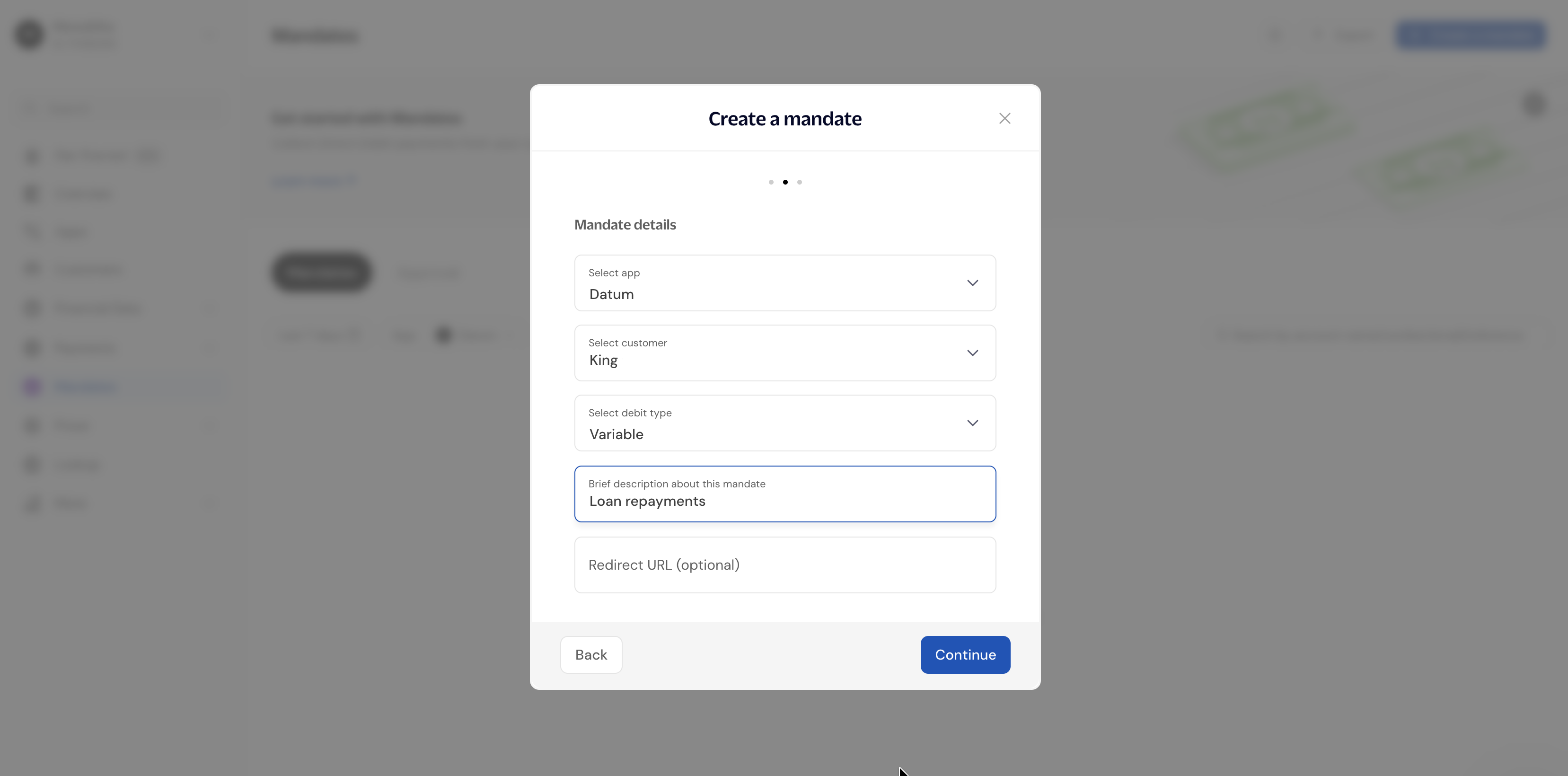

Fill in the required mandate details: the debit type, mandate description, preferred app, etc.

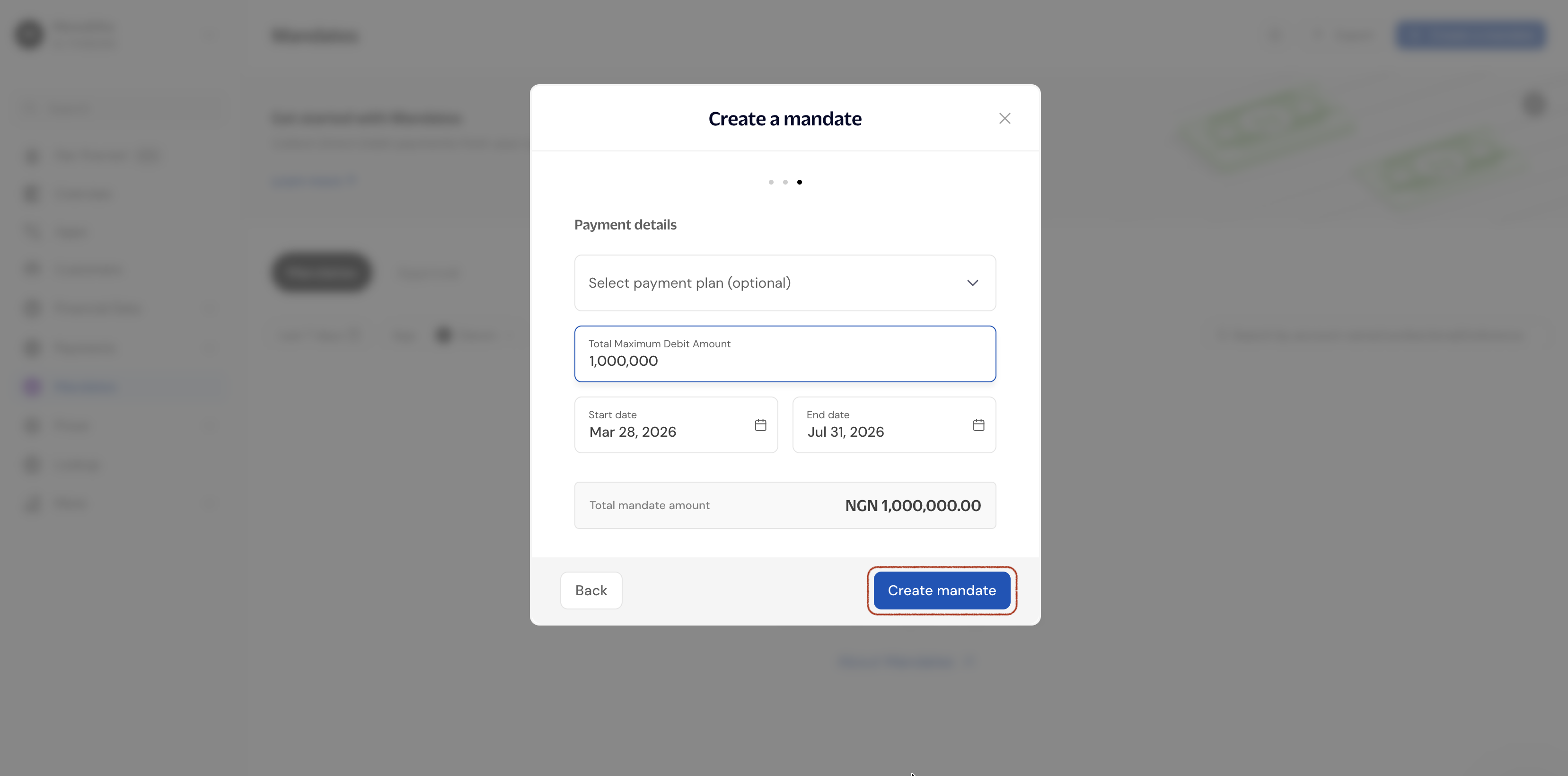

Next, add the mandate payment details, including the start and end dates, total debit amount, and chosen payment plan. Then click the Create mandate button to complete setup.

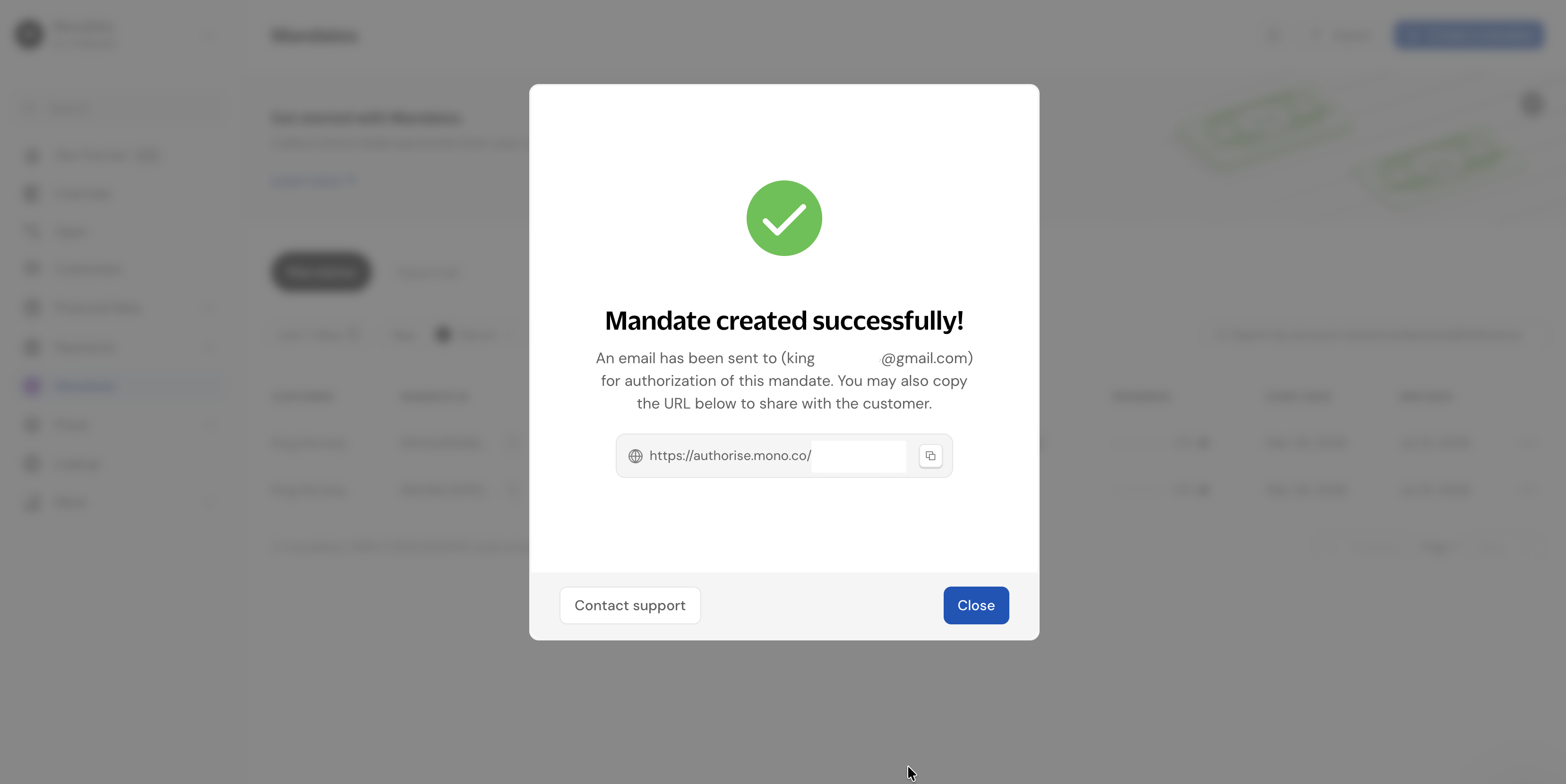

After the mandate is created successfully, a link will be automatically generated, and you can share it with the customer.

Questions you may have and answers to them

1. How is a customer’s consent obtained?

Customers approve mandates on their accounts and schedule debits through a transparent authorization flow. They have to verify account ownership using their login credentials and transfer a N50 authorization fee to a NIBSS account.

2. Can accounts be debited without authorization?

No, Mono Sweep operates strictly based on authorization from users.

3. How long does it take for a mandate to be approved?

Authorization for Mono Sweep works through e-mandates. So, the primary mandate and other linked mandates are approved within 3-7 minutes.

4. Is there a limit to linked accounts?

No. Mono sweep mandates are set up on supported bank accounts tied to a user’s BVN.